The Federal Reserve has just pledged to buy $40 billion in U.S. Treasury bonds per month, and the market is already chanting "quantitative easing (QE)." While on the surface this figure seems like a signal to stimulate the economy, the underlying mechanism tells a different story. Powell's move is not to stimulate the economy, but to prevent problems from occurring in the financial system.

The following is an analysis of the structural differences between the Federal Reserve's Reserve Management Purchases (RMP) program and quantitative easing (QE), as well as its potential impact.

What is quantitative easing (QE)?

In order to strictly define quantitative easing and distinguish it from standard open market operations, the following conditions need to be met:

Three major mechanical conditions

- Mechanism (asset purchase) : The central bank purchases assets, usually government bonds, by creating new reserve funds.

- Scale (Large-scale) : The purchase volume is significant relative to the total market size, and its purpose is to inject a large amount of liquidity into the system rather than to make fine adjustments.

- Objective (Quantity over Price) : Standard policy achieves a specific interest rate (price) target by adjusting supply, while quantitative easing purchases a specific quantity of assets (quantity), regardless of how the interest rate ultimately changes.

Functional conditions

- Positive net liquidity (QE) : The pace of asset purchases must exceed the growth rate of non-reserve liabilities (such as monetary and Treasury general accounts). Its goal is to force excess liquidity into the system, rather than simply providing the necessary liquidity.

What is Reserve Management Purchase (RMP)?

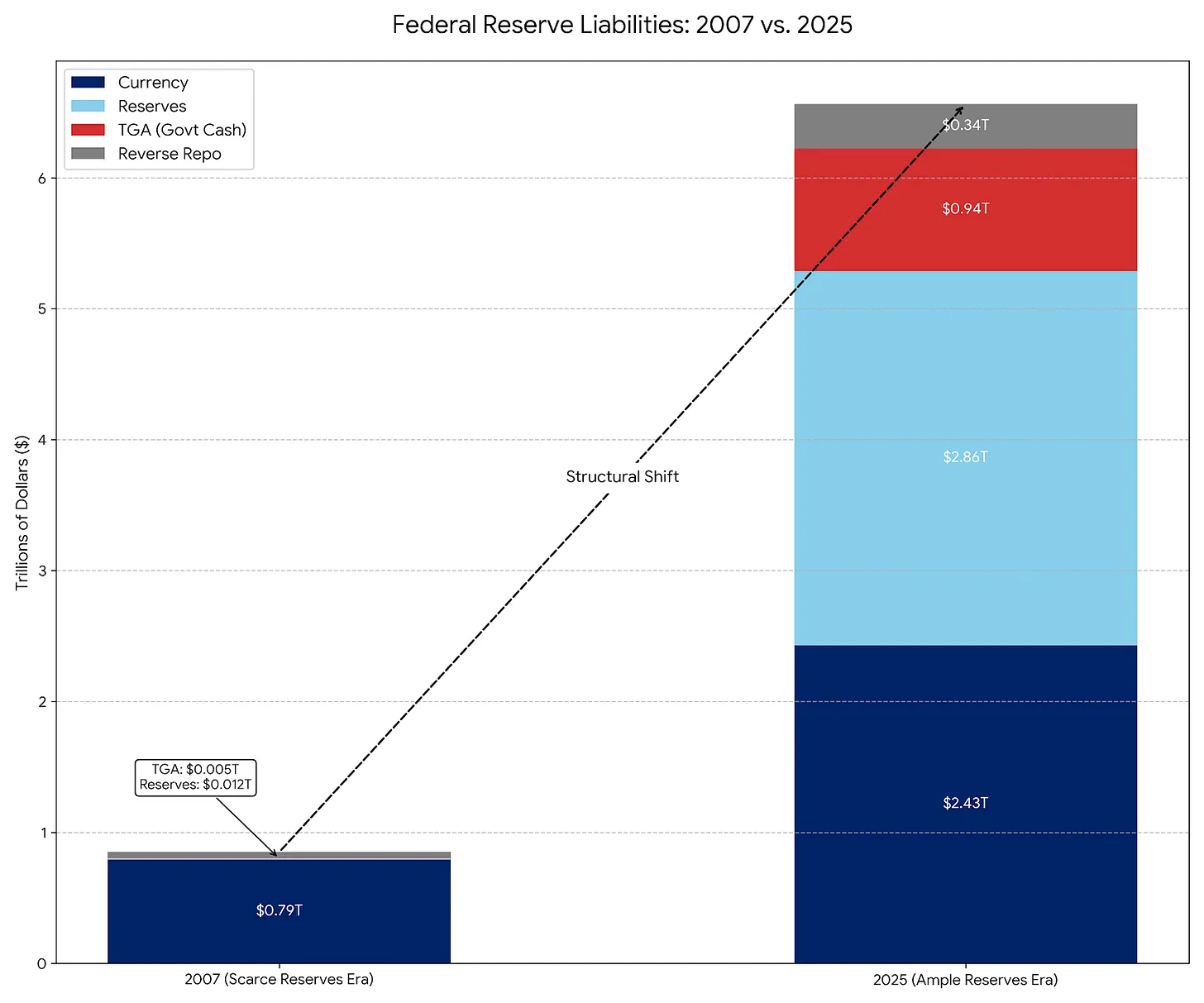

The RMP is essentially a modern successor to Permanent Open Market Operations (POMO), which was the standard operating procedure from the 1920s to 2007. However, since 2007, the composition of the Federal Reserve's liabilities has changed dramatically, necessitating adjustments to the scope of operations.

POMO (Scarcity Reserve Era)

Prior to 2008, the Federal Reserve's primary liability was physical currency in circulation; other liabilities were fewer and more predictable. Under POMO (Provisional Transaction Management), the Fed purchased securities solely to meet the public's gradual demand for physical cash. These operations were calibrated to liquidity neutrality and were small in scale, avoiding market price distortions or yield depression.

RMP (Era of Ample Reserves)

Currently, physical currency constitutes only a small portion of the Federal Reserve's liabilities, which are primarily dominated by large and volatile accounts such as the Treasury General Account (TGA) and bank reserves. Under the Reserve Requirement Plan (RMP), the Fed purchases short-term Treasury bills (T-Bills) to cushion these fluctuations and "maintain an adequate supply of reserves." Similar to the Procurement of Ministries (POMO), the RMP is designed to be liquidity-neutral.

Why launch RMP at this time: The impact of TGA and tax season

Powell implemented the Reserve Management Purchase Program (RMP) to address a specific financial system problem: the TGA (Treasury General Account) liquidity drain.

How it works : When individuals and businesses pay taxes (especially during the major tax deadlines in December and April), cash (reserve funds) is transferred from their bank accounts to the Federal Reserve’s Government Checking Account (TGA), which is located outside the commercial banking system.

Impact : This transfer of funds will drain liquidity from the banking system. If reserves fall too low, banks will stop lending to each other, potentially triggering a repo market crisis (similar to the situation in September 2019).

Solution : The Federal Reserve is now launching the Reserve Flow Management (RMP) to offset this liquidity withdrawal. They are doing so by creating $40 billion in new reserves to replace the liquidity that will soon be locked in the Total Gains Market (TGA).

Without RMP : Tax payments would tighten financial conditions (negative). With RMP : The impact of tax payments is neutral (neutral).

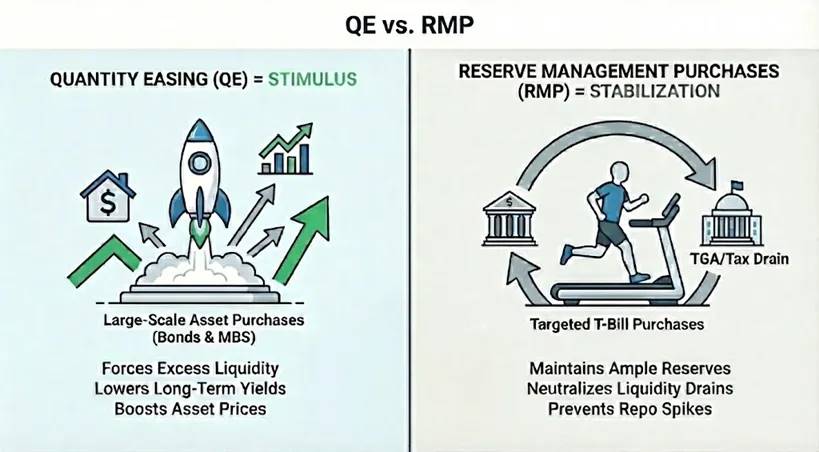

Is RMP actually QE?

Technically speaking : Yes. If you're a strict monetarist, the RMP meets the definition of QE. It satisfies the three mechanical conditions: large-scale asset purchases through new reserves (US$40 billion per month), and the focus is on quantity rather than price.

Functionally : No. The role of the Reserve Measure (RMP) is to stabilize, while the role of QE is to stimulate. The RMP does not significantly loosen financial conditions, but rather prevents further tightening of financial conditions during events such as TGA replenishment. Because the economy itself will naturally withdraw liquidity, the RMP must continue to operate to maintain the status quo.

When will RMP transform into true QE?

The transition from RMP to full QE requires a change in one of the following two variables:

A. Changes in duration : If the RMP begins purchasing long-term Treasury bonds or mortgage-backed securities (MBS), it becomes QE. By doing so, the Fed removes interest rate (duration) risk from the market, lowers yields, forces investors to shift to riskier assets, and thus pushes up asset prices.

B. Changes in Quantity : If the natural demand for reserves slows (e.g., TGA stops growing), but the Federal Reserve continues to purchase $40 billion per month, the RMP becomes QE. In this case, the Federal Reserve is injecting liquidity into the financial system beyond what is needed, and this liquidity will inevitably flow into the financial asset markets.

Conclusion: Market Impact

The Repurchase Agreement (RMP) aims to prevent liquidity withdrawals during tax season from impacting asset prices. While technically neutral, its reintroduction sends a psychological signal to the market: the "Fed Put" has been activated . This announcement is net positive for risk assets, providing a "mild tailwind." By committing to $40 billion in monthly purchases, the Fed effectively provides a floor for liquidity in the banking system. This eliminates the tail risk of the repurchase crisis and strengthens market confidence in leverage.

It is important to note that the RMP is a stabilizer, not a stimulant. Since the RMP merely replaces the liquidity withdrawn by the TGA, rather than expanding the net monetary base, it should not be mistaken for a true form of systemic easing under QE.