Written by: shushu,BlockBeats

On June 18, the U.S. Senate officially passed the GENIUS Act, marking the first time the U.S. government legally recognized the compliance legitimacy of crypto assets, breaking the policy vacuum caused by the previously ambiguous regulatory rights of the SEC and CFTC.

Against this regulatory backdrop, JPMorgan and Coinbase simultaneously announced major developments, focusing on on-chain banking services and tokenized securities, demonstrating the deep integration of traditional finance and the crypto ecosystem.

JPMorgan's deposits can now be placed on Base

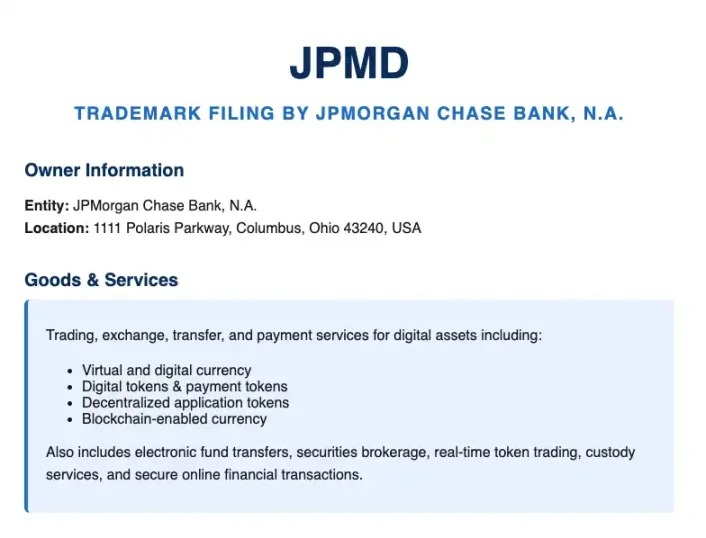

JPMorgan, the most early and proactive in blockchain deployment among traditional financial institutions, announced the launch of a pilot project called JPMD (JPMorgan Deposit Token). JPMD is an on-chain token representing clients' U.S. dollar bank deposits, based on a fractional reserve mechanism, and will be deployed on Base, the public chain supported by Coinbase.

Naveen Mallela, co-head of JPMorgan's blockchain division Kinexys, stated that the bank will complete the first JPMD transfer within the next few days, moving funds from its digital wallet to the Coinbase platform, paving the way for subsequent institutional client use of the token for on-chain transactions.

The pilot is expected to last several months, marking JPMorgan's further exploration of efficient and secure institutional-level trading tools through on-chain deposit tokens. The day before, the bank had applied for the "JPMD" trademark, covering digital asset payment, transfer, and trading services, indicating its long-term application intentions.

JPMorgan's choice to pilot JPMD on Base not only demonstrates its recognition of Base's security and transaction efficiency but also means that future institutional clients may directly conduct on-chain fund settlement through Base and the Coinbase ecosystem, injecting core liquidity into Coinbase's "CeDeFi bridge".

Why "deposit tokens"?

Although the launch of JPMD has sparked market speculation about its potential entry into the stablecoin market, Naveen Mallela from JPMorgan's blockchain division Kinexys told Bloomberg that deposit tokens are a better alternative to stablecoins for institutional users due to their fractional reserve mechanism, which offers greater scalability.

He pointed out that deposit tokens represent actual U.S. dollar deposits in customer bank accounts, operating within the traditional banking system. In contrast, stablecoins are merely digital mappings of fiat currency supported by cash and equivalents, with a legal status and operating logic more detached from the traditional financial system.

Simultaneously with the JPMD pilot launch, three core executives from JPMorgan have engaged in closed-door talks with the SEC's crypto special working group, discussing how capital market tools can migrate to public chains, the potential impacts on market structure, and how institutions should assess risk control and revenue models in on-chain finance.

According to the SEC's meeting minutes, the discussions covered multiple cutting-edge directions, including digital repurchases, digital debt instruments, and on-chain financing. JPMorgan also clearly stated that it is actively evaluating whether it can form a structural competitive advantage in asset tokenization and on-chain settlement efficiency.

Besides "chasing on-chain meme", stocks can also be bought on Base

Echoing JPMorgan's exploration of the on-chain banking system, Coinbase is also evolving from a trading platform to an on-chain asset infrastructure provider. The company's Chief Legal Officer, Paul Grewal, revealed that Coinbase is applying to the U.S. SEC for a no-action letter to offer tokenized stock trading services to U.S. customers, subject to exemption or permission. If granted, it means SEC staff will not take enforcement action against Coinbase's tokenized stock service.

If Coinbase successfully obtains approval for its tokenized stock business, it will be the first to achieve an integrated asset circulation closed loop of "stablecoin purchase → on-chain settlement → stock trading → cashback consumption" on the same platform. This not only challenges the trading entry positions of Robinhood and Charles Schwab but may also force these platforms to consider introducing stablecoin payment and on-chain settlement logic, pushing the entire securities industry into the on-chain asset era.

Tokenized stocks promise faster settlement speeds, longer trading time windows, and lower operating costs. However, U.S. investors currently cannot access such products. Coinbase's new plan means it will not only be the "NASDAQ" of crypto assets but also become the on-chain entry point for traditional securities trading.

In fact, this is not Coinbase's first exploration of tokenized stocks. As early as the S1 filing stage before the company's IPO in 2021, it had planned to tokenize its own stock COIN but ultimately shelved the plan due to lack of SEC approval.

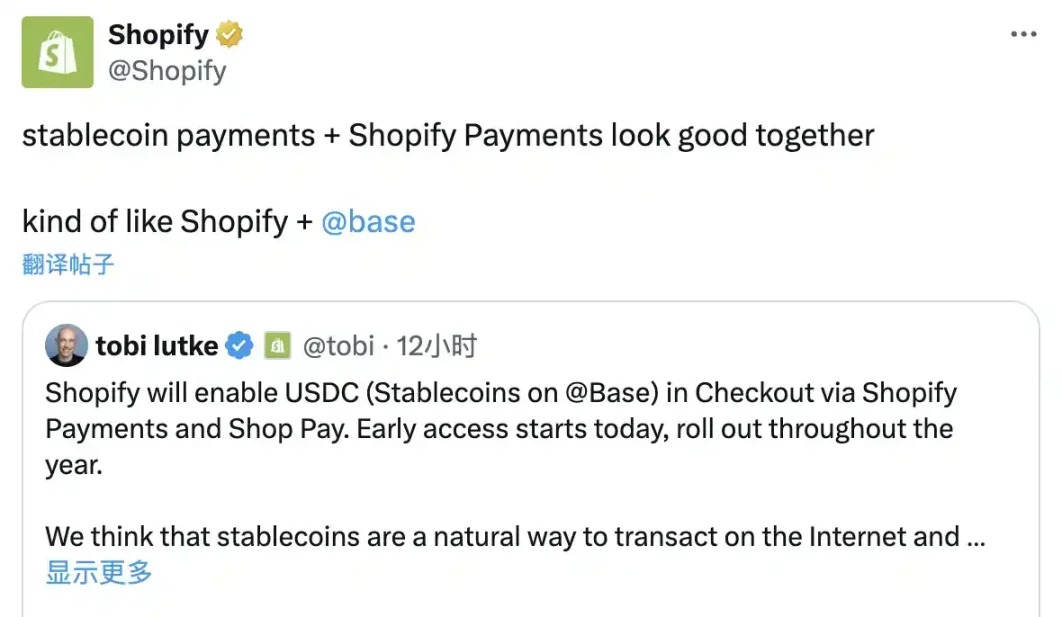

This attempt is Coinbase's latest move to expand beyond crypto assets, aiming to open up new revenue sources and drive further institutional adoption. Just last week, Coinbase launched a credit card supported by American Express and collaborated with Shopify and Stripe to promote USDC stablecoin payments.

Regulatory uncertainty has long been the main barrier to widespread blockchain securities trading adoption. However, with the SEC's adoption plans for DeFi and stablecoins, regulation is no longer a concern for Coinbase.

Meanwhile, competition is intensifying. Coinbase's announcement of tokenized stocks follows Kraken's xStocks project, which has begun offering on-chain trading services for over 50 stocks and ETFs in European, Latin American, African, and Asian markets. Coinbase needs faster and clearer regulatory channels to compete in the new crypto brokerage race.

All for Revenue

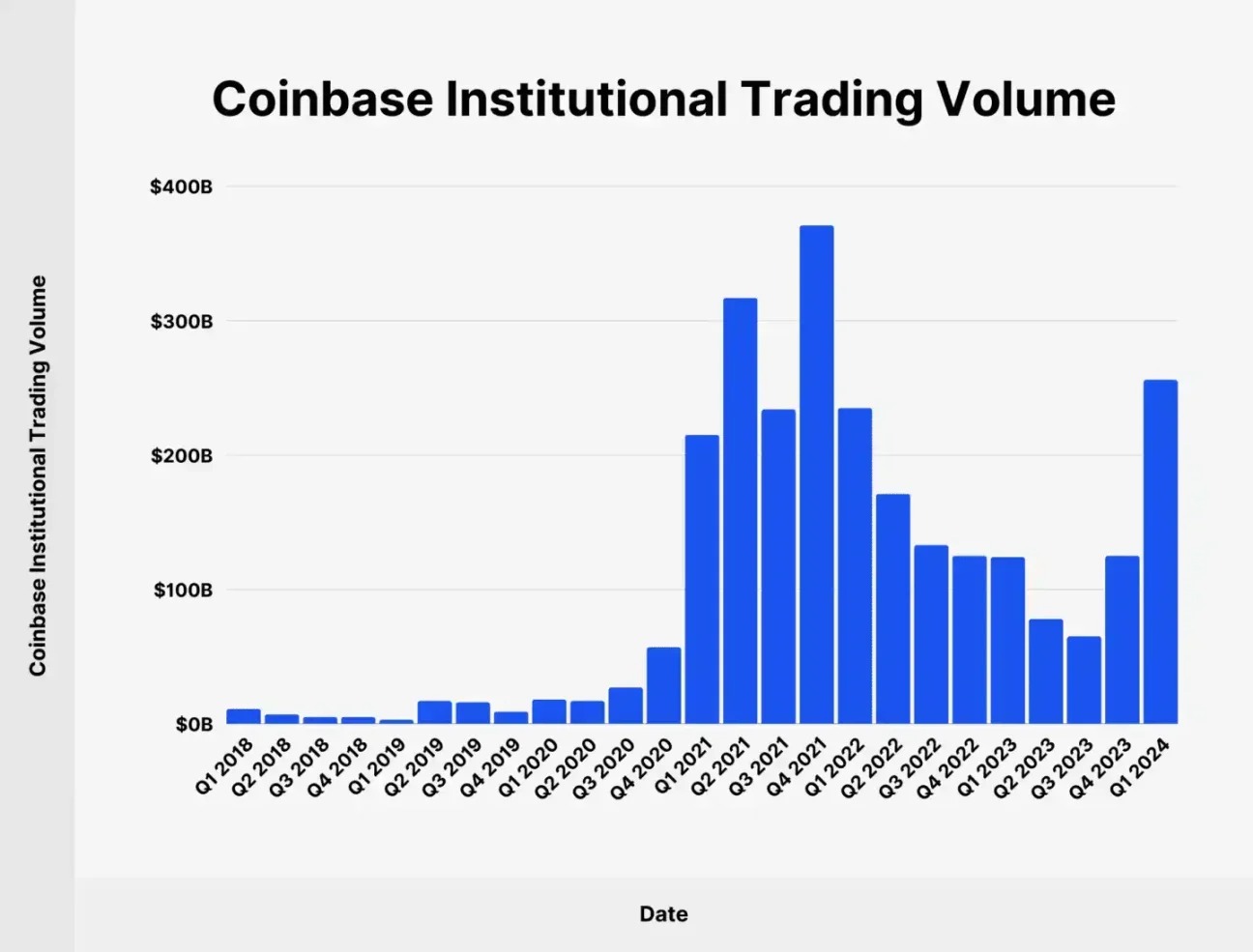

Statistics show that retail trading accounts for only about 18% of Coinbase's transactions. Since 2024, institutional client trading volume has been continuously increasing (Q1 2024 trading volume was $256 billion, accounting for 82.05% of total trading volume). With Coinbase's integration of DEX on Base, it should be able to introduce significant liquidity for tens of thousands of Base chain tokens, and more importantly, many Base ecosystem products will have the possibility of a compliant pathway through Coinbase.

This month, Coinbase has simultaneously collaborated with Shopify to support USDC payments on Base during e-commerce checkout, entering cross-border stablecoin payments; integrated Base's DEX into its main app, connecting on-chain assets with CeFi users; and most disruptively, announced the launch of 24/7 perpetual contract trading functions in the U.S. that comply with the CFTC regulatory framework.

These actions collectively point to a core objective - rebuilding Coinbase's revenue model. As spot trading revenue declines year by year, Coinbase's financial reports show an over-reliance on crypto market cycles. In this context, derivatives become a more counter-cyclical income source. By integrating Deribit's liquidity and user base, Coinbase is constructing a global institutional derivatives trading closed loop, with CFTC endorsement providing a compliant moat in the U.S. market.

Simultaneously, Coinbase is promoting USDC's native use in e-commerce payment scenarios through collaborations with Shopify and Stripe. Consumers can directly use USDC for checkout at Shopify stores, while merchants can choose to settle in stablecoins or local currency. Combined with smart contract custody and API modules on Base, this process requires no crypto knowledge from consumers or merchants, forming a highly scalable "compliant crypto payment engine". Stablecoin transactions not only bring on-chain gas fees and settlement charges but also open up stable income channels for Coinbase in long-tail markets like small businesses and cross-border e-commerce.

The Coinbase One Card's collaboration with American Express uses cashback as a hook, binding users through asset lock-up to further activate platform trading behavior. Although such products currently need to balance costs and returns, they reflect Coinbase's strategy of gradually integrating "financial services + consumption scenarios".

This rhythmic multi-point strike is not coincidental. During the window period of emerging regulatory benefits and gradually improving on-chain settlement infrastructure, Coinbase chooses to use its own platform as a hub, building a multi-dimensional revenue network centered on compliance and characterized by diverse asset liquidity, spanning from DEX and stablecoin payments to derivatives trading. Behind this logic lies the critical inflection point of Coinbase's transformation from a crypto exchange to an on-chain financial operating system.

Whether it's JPMD issued based on bank deposits by JPMorgan Chase or Coinbase's layout for a tokenized securities platform, both point to the same trend - on-chain finance is entering a period of institutional reconstruction driven by regulation, infrastructure, and mainstream financial institutions.

The passage of the 'GENIUS Act', the heating up of stablecoin discussions, and continuous experiments by major institutions in on-chain market infrastructure mean that crypto finance is no longer a marginal experiment, but a realistic choice gradually embedded in the global financial market structure, with the boundaries between on-chain and off-chain being progressively broken down by these pioneers.